At the beginning of 2017, payment orders for insurance premiums changed. The BCC, recipient details, and other values have changed in the payments. However, we have good news: tax authorities will correct many errors automatically without statements from accountants.

If you sent insurance premiums to the old fund details

From January 1, 2017, insurance premiums must be transferred to the Federal Tax Service, and not to funds (federal laws of July 3, 2016 No. 243-FZ and No. 250-FZ). This also applies to payments for previous years. For this reason, the BCC and details of the recipient of insurance premiums have changed in your payments. Let's assume that at the beginning of the year you made a mistake and filled out the payment order incorrectly, for example, instead of the TIN, KPP and the name of the tax office, you entered the fund's data. Then the tax authorities will correct the payments automatically. And you will not need to contact officials with a request to clarify the payment or return the money.

Tax officials and the Federal Treasury promise to automatically recode incorrect payments, correct old BCCs with new ones, change the recipient of contributions (joint letter of the Federal Tax Service of Russia dated January 17, 2017 No. ZN-4-1/540 and the Treasury of Russia dated January 16, 2017 No. 07-04-05/ 05-46).

Payments that you mistakenly sent to the funds will still go to the tax authorities. And you will not have to pay penalties and fines for late payment of fees. Inspectors will reflect the money when you actually sent it. But if you want to correct your payments as quickly as possible, you have the right to contact the tax office with a request to clarify bank orders. See below for a sample application.

If you made a mistake in the payer status (field 101)

In 2017, accountants had difficulties with field 101 “Payer Status” of payment orders for contributions. In 2016, when paying insurance premiums for employees, companies and individual entrepreneurs reflected status 08 in this field. This code is provided for insurance premium payers in the rules for filling out orders (Appendix No. 5 to Order No. 107n of the Ministry of Finance of Russia dated November 12, 2013). Officials did not make any changes to the procedure for filling out payment slips. Due to the fact that tax authorities began to control contributions, accountants began to question whether the payer’s status had changed since 2017.

Officials have issued several conflicting explanations. At first they recommended indicating status 08 in field 101. Then information appeared that it was necessary to reflect status 14 (joint clarification dated January 26, 2017 by the Federal Tax Service of Russia No. BS-4-11/1304@, the Board of the Pension Fund of the Russian Federation No. NP-30-26/947 and the FSS RF No. 02-11-10/06-308-P). However, many banks do not accept payment orders with a value of 14. Therefore, tax officials advised companies to enter in field 101 the status provided for tax payers - 01 (letter of the Federal Tax Service of Russia dated 02/03/2017 No. ZN-4-1/1931@).

Whatever status you specify, the payment will still go to the budget. There is no need to specify the payment. Moreover, officials and banks have not yet agreed on which value is correct.

Banks promise to finalize the software so that they allow payment of insurance premiums for employees with status 14. Until this happens, indicate the value 01 (employee contributions) or 09 (individual entrepreneur contributions). Payments with status 08 will also go through.

Errors in payment and how to correct them?

| Error | What to do |

|---|---|

| Incorrect Russian Treasury account number and recipient bank details | Tax inspectors will consider insurance premiums unpaid. The Federal Tax Service will demand payment of the arrears with penalties and fines and will block the account (clauses 4, 6 and 8 of Article 45 of the Tax Code of the Russian Federation). You will have to pay the fees again using the correct details. Return the erroneous payment. To do this, contact:

|

Incorrect details:

|

The money arrived as intended. Check your payment by submitting an application to the tax office with the correct details |

| You transferred an excess amount of insurance premiums to the budget | You can offset the overpayment against future payments. Another option is to return the overpayment. To do this, submit an application. Before offset or return, the Federal Tax Service of Russia may order a reconciliation of settlements |

| Confused FSS, PF and IFTS | The situation when you sent contributions to the funds to the old details, and not to the Federal Tax Service, is not dangerous. In this case, tax authorities will recode the payment to the correct details automatically. |

Nuances requiring special attention

If you sent insurance premiums to the old details of the funds, and not to the tax authorities, the Federal Tax Service will automatically recode the payments. In this case there is no delay in payment of contributions.

You have the right to clarify the payment by submitting an application to the Federal Tax Service. Enter the details of the payment order in which errors were made. Please indicate what you want to correct.

Banks do not allow payments for contributions with status 14. Therefore, indicate status 01 or 09.

Sample application for clarification of payment

| To the head of the Federal Tax Service No. your tax office in the Vladimir region (what region is yours) From the name of your legal entity INN 330812300601/ KPP 3301001 Address: your legal address |

||

| APPLICATION for clarification of payment | ||

|

By payment order No. 10 dated 02.02.2017, Progress LLC paid pension insurance contributions for January 2017 in the amount of 10,000 rubles. By mistake, the company reflected the KBK for 2016 in the payment. Payment of pension insurance contributions was made in 2017. Therefore, the code should be - 182 1 02 02010 06 1010 160. Please: | ||

You can clarify your tax payments according to the rules prescribed in Art. 45 of the Tax Code of the Russian Federation. Thus, this norm establishes that if a taxpayer discovers an error in the execution of an order for the transfer of tax, which does not entail the non-transfer of this tax to the budget, he has the right to submit to the tax authority at the place of his registration an application about the error with the attachment of documents confirming his payment of the specified tax and its transfer to the appropriate account of the Federal Treasury, with a request to clarify the basis, type and identity of the payment, tax period or payer status.

From 12/01/2017, the procedure for the work of tax authorities with unclear payments (hereinafter referred to as the Procedure) comes into force.In this regard, in the article we propose to consider the mechanism of interaction between the Federal Tax Service and the taxpayer in a situation where errors were discovered in the payment order for the transfer of taxes to the budget.

In accordance with clause 1 art. 45 Tax Code of the Russian Federation The taxpayer (including legal entities and individual entrepreneurs) is obliged to independently fulfill the obligation to pay tax, unless otherwise provided by the Tax Code of the Russian Federation, within the period established by law. Failure to fulfill (improper fulfillment) of the obligation to pay tax is the basis for the tax authority to send a demand for tax payment to him.

On the fulfillment and non-fulfillment of the obligation to pay tax

Taxpayers must prepare settlement documents for the transfer of taxes (fees) and other payments to the budget system of the Russian Federation in accordance with Order of the Ministry of Finance of Russia dated November 12, 2013 No. 107n “On approval of the Rules for indicating information in the details of orders for the transfer of funds for payment of payments to the budget system of the Russian Federation" (hereinafter - Rules No. 107n).According to pp. 1 clause 3 art. 45 Tax Code of the Russian Federation duty to pay tax is considered fulfilled from the moment of presentation to the bank of an order to transfer funds to the budget to the appropriate account of the Federal Treasury from the taxpayer’s bank account if there is a sufficient cash balance on it on the day of payment.

By virtue of clause 7 art. 45 Tax Code of the Russian Federation the tax transfer order is filled out in accordance with the rules established Regulations on the rules for transferring funds.

Subclause 4 of clause 4 of Art. 45 Tax Code of the Russian Federation a number of cases have been established when the obligation to pay tax is not considered fulfilled . These include, in particular, incorrect indication by the taxpayer in the order to transfer the amount of tax:

Federal Treasury account numbers;

The name of the recipient's bank, which resulted in the non-transfer of this amount to the budget.

Moreover, if the payment order incorrectly indicates the BCC or the status of the tax payer, this is not a basis for recognizing the obligation to pay tax as unfulfilled (letters Ministry of Finance of Russia dated January 19, 2017 No. 03‑02 ‑07/1/2145 , Federal Tax Service of Russia dated October 10, 2016 No. SA-4-7/19125@).

Thus, if the taxpayer’s mistake did not lead to non-payment of tax, then he has the right to clarify his payment. The procedure for clarifying an unclear payment is specified in clause 7 art. 45 Tax Code of the Russian Federation.

How do tax authorities deal with uncleared payments?

Unexplained payments include:Payments based on settlement documents in the fields of which information is not indicated (incorrectly indicated) by the taxpayer (or by the bank when generating an electronic payment document);

Payments that cannot be clearly identified for reflection in the information resources of tax authorities.

All information about working with outstanding payments is collected in the statement of outstanding receipts. In it, tax authorities reflect:

Payments attributed by the treasury to the appropriate BCC for accounting for unidentified receipts;

Payments processed by taxpayers in violation Rule No. 107n, which led to the impossibility of reflecting them in cards of settlements with the budget or information resources of tax authorities, which record the corresponding revenues;

Payments that cannot be clearly classified to be reflected in the cards of specific taxpayers;

Payments for which taxpayers do not have budget payment cards open.

Do you want to clarify your payment? Report this to the Federal Tax Service!

Clause 7 of Art. 45 Tax Code of the Russian Federation set: when detected taxpayer errors in the execution of an order for the transfer of tax, which did not entail (!) the non-transfer of this tax to the budget, he has the right to submit a statement of error to the inspectorate at the place of his registration.The document submitted to the tax authorities must contain a request to clarify the basis, type and origin of the payment, tax period or payer status. Documents confirming the payment made must be attached to the application.

Feedback from tax authorities

The need to clarify the payment (in terms of clarifying the details of the payment document) in order to correctly reflect information about it in the resources of the Federal Tax Service may also arise from tax authority . In this case, the inspectorate itself will inform the taxpayer about this.The form of the corresponding information message is presented in Appendix 2 to Order. In the message, the controllers will indicate that the order to transfer tax was issued in violation of the established Rules No. 107n requirements, and the specific violation committed by the taxpayer will be named. Violations may be of the following nature:

Absence or indication of a non-existent (incorrect) KBK, OKTMO code;

The payer's TIN is not indicated (incorrectly indicated);

TIN does not match the name of the payer;

Absence or incorrect indication of the payer’s checkpoint;

Indication of a non-existent (incorrect) TIN of the recipient;

Absent, a non-existent (incorrect) recipient checkpoint is specified;

The taxpayer is not registered with the tax authority;

Tax payment is made for third parties;

Absence or incorrect indication of the basis for payment or the recipient's account number and name;

Lack of an open payment card with the taxpayer’s budget;

absence or incorrect indication of the payer status and tax period.

After receiving an information message about the need to clarify the details of the order for tax transfer, the payer submits to the inspectorate a statement about the need for this clarification.

When the tax authority receives an application from the taxpayer to clarify the type and nature of the payment, the tax authority, within 10 working days from the date of receipt of the said application, makes an appropriate decision (the application form has been approved By Order of the Federal Tax Service of Russia dated December 29, 2016 No. ММВ-7-1/731@).

For your informationAt the suggestion of one of the parties (inspectorate or taxpayer), a joint reconciliation of taxes paid by the taxpayer can be carried out.If an error in the payment document arose due to the fault of the bank when generating an electronic payment document, the tax authority, after reconciling settlements with the payer, has the right to make a request to this credit institution in order to obtain a copy of the payment document executed by the payer on paper.

The procedure for conducting reconciliation is regulated by clause 3 of the Order of the Federal Tax Service of Russia dated 09.09.2005 No. SAE-3-01/444@ “On approval of the Regulations for organizing work with taxpayers, payers of fees, insurance contributions for compulsory pension insurance and tax agents.”

The result of interaction with the INFS regarding unclear payments

Based on the taxpayer’s application and the act of joint reconciliation of calculations (if it was carried out), the inspectorate makes a decision to clarify the payment on the day of actual payment tax In this case, the tax authority recalculates the penalties accrued on the amount of tax for the period from the date of its actual payment to the budget until the day the Federal Tax Service Inspectorate makes a decision to clarify the payment.The taxpayer will be notified of the decision to clarify the payment within five days after the decision is made.

Clarification of details for payment of insurance premiums

The procedure for clarifying payment documents for insurance premiums is similar to the activities carried out by the inspectorate to clarify tax payments. However, if errors are detected in their documents, taxpayers should be guided by the following.Firstly , clarification of details in settlement documents for the payment of insurance premiums is not carried out if information about this amount is recorded on the individual personal account of the insured person. This is enshrined in clause 9 art. 45 Tax Code of the Russian Federation.

Secondly , the procedure for specifying details in payment documents depends on the date of payment.

If the payment is made for settlement (reporting) periods that have expired until 01/01/2017 , funds for which were received by the Pension Fund (before the transfer of administration of insurance premiums to the Federal Tax Service), then an application to clarify the details must be submitted to the Pension Fund branch.

The Pension Fund of Russia will review it within five working days and make an appropriate decision, which will be sent to the Federal Tax Service. Simultaneously with this decision, the amount of penalties subject to reduction or additional accrual, recalculated as of 01/01/2017, is also transferred. Based on the information received from the Pension Fund of Russia, the tax authorities will reflect the decision and the amount of the penalty in the payer’s personal account.

If the funds have arrived after 01/01/2017 , then the application must be submitted to the tax office. In this case, controllers send a request to the Pension Fund of the Russian Federation, attaching copies of the payer’s application and payment document.

The Pension Fund of Russia will review the application within five working days and send a message to the inspectorate about the possibility (or lack thereof) of taking appropriate measures to clarify the details. And the INFS, based on this message, will decide to clarify the payment. In this case, the recalculation of penalties will be carried out by tax authorities in an automated mode from the date of actual payment.

Tax legislation gives taxpayers the right to clarify with the Federal Tax Service their erroneous tax payments (as well as payments for insurance premiums), setting one condition: an error in the execution of a payment document for the transfer of tax (insurance contributions) should not result in non-transfer of funds to the budget.

Effective from 12/01/2017 Order of the Ministry of Finance of Russia dated July 25, 2017 No. ММВ-7-22/579@, which approved the procedure for tax authorities to work with unclear payments. From this date, controllers in interaction with taxpayers will be guided by the provisions of this document.

In addition, in order to correctly fill out payment documents, the Federal Tax Service plans to carry out large-scale work to inform taxpayers about the values of the details required to fill out the fields of payment documents by posting the relevant information on stands in territorial tax authorities. Information about the details of the relevant Federal Treasury accounts can be obtained from the Federal Tax Service and upon registration ( clause 6 art. 32 Tax Code of the Russian Federation). We also remind you that on the website of the supreme tax department you can find any details necessary for filling out payment documents.

A payment order is a payment document that has a unified form (0401060). Appendix No. 2 to the order of the Ministry of Finance of the Russian Federation dated November 12, 2013 No. 107n approved the rules for filling out the form. It is especially important to fill out the payment form correctly when transferring taxes and contributions. If an error was nevertheless made, then in a number of cases the taxpayer has the right to submit to the tax office an application to clarify the payment (clause 7 of Article 45 of the Tax Code of the Russian Federation).

Why is it not always possible to get by with a clarifying letter to the Federal Tax Service? The legislator gives the payer this opportunity only in cases where, despite a typo, the payment was received in the budget system of the Russian Federation to the appropriate account of the Federal Treasury. It turns out that if the recipient’s bank and the Federal Treasury account number are indicated correctly, and the typo is contained in other fields of the payment order, then it is quite possible to correct the erroneous data using an application to the tax office to clarify the payment.

Thus, the most dangerous details are:

- name of the recipient's bank;

- Russian Treasury account number.

IMPORTANT! Errors in them cannot be corrected.

Features of submitting an application to the tax office for clarification of payment

We list the key nuances of filing an application for clarification:

- For each incorrect payment order, a separate application is drawn up, but in duplicate.

- The sooner the organization corrects the inaccuracy in the payment, the less likely it is for further disputes with the tax authorities.

- The deadline for the tax inspectorate to make a decision on an application for clarification cannot be found in the Tax Code. In practice, tax authorities make a decision to clarify the payment within 5-10 days after receiving the application, and inform the taxpayer about this within 5 days.

- The taxpayer can submit an application directly to the Federal Tax Service. In this case, the second copy is given to the applicant with the tax stamp. It is also possible to send a letter by mail or through an electronic reporting operator.

We have selected excellent electronic reporting services for you!

Don't know your rights?

What does an application for clarification of payment look like (sample)

You will have to clarify the payment in any form, since there is no regulated one. But, according to paragraph 7 of Art. 45 of the Tax Code of the Russian Federation, it is required to attach a correctable payment order, duly certified by the bank.

An application for clarification of payment to the Federal Tax Service usually has a structure dictated by the rules of document management.

Basic instructions:

- The header contains information about the applicant company and the tax office to which the application is being submitted.

- The title of the letter follows. Wording may vary. For example, “application for clarification of tax payment.”

- In accordance with the organization's standards, the date and originating document number are given.

- The body of the letter contains information about the error (in which payment order what typos were made), as well as a request to clarify the payment and consider the new payment order details correct.

- The head puts a signature, which is certified by the seal of the organization (if any).

You can download a sample application for clarification of payment to the tax office using the link below:

If an organization made a non-critical error in a payment document and the obligation to pay tax was fulfilled, then an application to the tax office to clarify the payment will help correct the situation. The application is drawn up in free form. You can use the sample presented in this article.

Most errors in payments can be clarified by submitting an application for payment clarification. For example, TIN, KPP, OKTMO. But there are two fields in which information cannot be clarified. What to do in these cases and how to fill out an application for clarification of payment in 2019 - read in this article.

Attention! The following documents will help you process payments without errors:

It is convenient to work with documents in . It is suitable for organizations and individual entrepreneurs. The program will automatically generate and print all the necessary primary data. It also includes uploading transactions to 1C, automatic generation of any reporting, and much more.

What errors in a payment order can be corrected by clarifying the payment?

However, not all errors can be corrected in an order. In the table we will show which data can be clarified and which cannot.

Table. What errors in the payment can be clarified

Just two errors in a document cannot be corrected. This is an incorrect Treasury number and beneficiary bank name. Therefore, the company will have to re-introduce the payment to the budget and return the erroneous transfer upon application.

If mistakes were made in the recipient’s KBK, INN or KPP, the tax authorities will first send a notification to the Treasury. And based on the results of the department’s response, they will inform the company about the results of the clarifications. In total, they are given 10 working days for this.

Most often, errors occur in the KBK. And this is quite understandable. After all, even a typo in one number is already an unreliable detail. For example, instead of KBK for contributions, they wrote down for personal income tax - 182 1 01 02010 01 1000 110 . Then that’s right, enter the code - 182 1 02 02010 06 1000 160 .

Companies also make mistakes in the TIN/KPP of the payer and recipient of money, status in field 101, purpose of payment, etc. These shortcomings can be corrected, the Federal Tax Service and the Pension Fund reported this in a joint letter dated 06.06.2017 No. 3N-4-22/10626a/ NP-30-26/8158.

Payment clarification in 2019: sample

Due to an error in the payment slip, the payment falls into the “unclarified” category, which means that there will be an arrears on the card and penalties will be charged. If the error can be corrected, submit a payment clarification request as soon as possible. The algorithm is as follows.

Step 1. Complete an application for payment clarification. There is no official form for the document, so you can compose it arbitrarily. In the header, write down the company details: name, INN, OGRN, address and telephone number so that inspectors can contact you. Next, on the right edge of the letter, indicate the details of the inspection where you are submitting your application. In this case, it is enough to write down: name and full name. head of the Federal Tax Service.

Place the title of the document in the center. For example, “Application for clarification of payment.” And only then, below in the text, explain in detail what exactly the company did wrong and how the details will be recorded correctly.

Step 2. Submit an application to the inspectorate. You can do this in several ways:

– submit the document in person to the Federal Tax Service;

– send the document by courier;

– by registered mail with acknowledgment of delivery;

- through the Internet.

The company can choose any method of sending a letter; there are no restrictions in the code. The only thing is that when sending a document via the Internet, sign it with an electronic digital signature. Then the file will be considered reliable.

The company must record all outgoing letters in a journal; an application for clarification of payment is no exception. Therefore, assign a serial number and date to the document when you send the document to the inspectors. Then reflect the details in the journal.

Step 3. Check the budget settlement card . Inspectors must respond to the application within 5 working days. Moreover, if their decision is positive, then they will reverse the penalty on the date when you actually sent the payment (clause 7 of Article 45 of the Tax Code of the Russian Federation). But if controllers have questions, they will ask for reconciliation of calculations and additional explanations. Therefore, the procedure for clarifying payment may take a long time.

The company can order a reconciliation at any time. To do this, submit an arbitrary application to the Federal Tax Service with a request to provide a certificate of settlements with the budget. You can submit your application on paper, but it’s faster to do it through an ED operator or your personal account on the Federal Tax Service website.

How to fill out a payment order in accounting programs

Instructions - how to fill out a payment form in Bukhsoft Online, 1C: Enterprise and Kontur.Accounting.

Bukhsoft Online

1. Go to the “Accounting” module and select the “Service/Our Accounts” section. Click "Change" and enter your bank details. After that, click the “Basic” button.

2. In order for the payment order to reflect the details of the recipient’s bank, you need to add a bank in the directory of counterparties, in the “Current Accounts” tab, then place the cursor on the line with the bank and click the “Main” button.

3. In the “Accounting” section, go to “Bank”. In the selection window, select the bank where you are sending the payment. Select a period and click Add. Fill out the form that opens. Save.

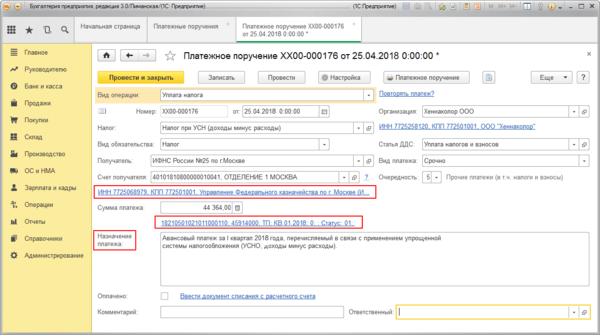

1C:Enterprise

1. Go to the menu: Bank and cash desk/Bank/Payment orders.

2. Click “Create”, select the type of transaction “Tax payment”.

3. Fill in all the necessary details using the hyperlinks in the “Payment Order” document.

4. Save the document using the “Save” button.

5. To output the document in printed format, click “Payment order”.

Kontur.Accounting

1. Start creating payment documents from the “Requirements” page. P Follow the “Pay” link.

2. Enter your bank details and payment amount. The payment amount can be corrected. You can specify the type of payment, and the remaining data is distributed automatically in the appropriate fields of payment documents. In addition to the standard payment order, you will be able to generate receipts for which you will transfer money to the Bank of Russia during a personal visit.

3. The finished tax payment slip can be saved in word format, and then printed and paid at the bank. You can also generate a special text file and upload it to your online bank.

A letter to the tax office to clarify a payment is a specialized template for contacting the Federal Tax Service with a request to correct incorrect details in a payment document. In this article we will tell you in what cases you can correct an inaccuracy in a payment order, as well as how to do it correctly.

What errors can be corrected?

The variety of fiscal taxes and fees often leads to the fact that the taxpayer makes typos in payment documents. If the error is not corrected, the payment may be lost, and the tax authorities will recognize the debt and apply penalties.

If an inaccuracy was identified before the payment document was executed by the bank or Federal Treasury authorities, the payment order can be recalled. But what to do if the payment order (PO) has already been posted and the funds have been debited from the current account in favor of the Federal Tax Service.

You can correct a payment order from 01/01/2019 due to any errors, but subject to three conditions:

- The statute of limitations has not expired, that is, three years have not yet passed since the transfers were made to the Federal Tax Service.

- The money was credited to the budget, that is, it went to the personal account of the Federal Treasury.

- When adjusting payment, no arrears are created for a specific tax liability.

In this case, you will have to prepare a sample: an application to the tax office to clarify the payment. However, not all errors can be corrected. Let's define the key conditions.

It is impossible to correct the PP for insurance contributions to the Federal Tax Service, as well as for contributions for injuries to the Social Insurance Fund, if:

- the money has not been received to the appropriate account of the Federal Treasury, that is, fields 13 and 17 (bank and beneficiary account) are filled in incorrectly in the payment order;

- an error was made in the KBK (the first three digits of the budget classification code are incorrectly indicated) in field 104;

- payment of the contribution to compulsory pension insurance was credited to the individual pension account of the employee (insured person), that is, the contributions already credited cannot be clarified (clause 9 Art. 45 Tax Code of the Russian Federation).

In other cases, the taxpayer can correct any errors and inaccuracies in the following fields of the PP:

How to fix the error

There is no unified sample - clarification of payment to the tax office. Therefore, you will have to prepare a written appeal in any form.

If the company has approved letterhead, then the letter can be written on it. Follow the basic rules of business correspondence when preparing your appeal. The application form for clarification of payment to the tax office must contain the following details:

- Date, number, amount of the payment order in which the inaccuracy was identified.

- Enter the purpose of payment for the incorrect payment order.

- Indicate the field in which there was a typo, error, or indicate the value of the incorrect attribute.

- Then write down which value for this attribute will be correct.

To the completed application form for clarification of payment to the tax office, attach a copy of the payment order in which incorrect information was identified.

If, due to an error in the payment, representatives of the Federal Tax Service assessed penalties, they may be cancelled. After reviewing your application, tax officials must decide whether to clarify the payment or not. If the decision is positive, then the accrued penalties will be reversed (clause 7 Art. 45 Tax Code of the Russian Federation, clause 12 art. 26.1 of Law No. 125-FZ, clause 11 of Art. 18 of Law No. 212-FZ as amended, in force until 01/01/2017, Letter of the Federal Tax Service No. ZN-4-22/10626a, Pension Fund of the Russian Federation No. NP-30-26/8158 dated 06/06/2017).

Sample application form for clarification of payment to the tax office for 2019

After we have drawn up a sample - a letter to the tax office about clarification of payment, we will move on to another type of business correspondence: not with the Federal Tax Service, but with the Social Insurance Fund.

Correcting errors in FSS payments

To correct an inaccuracy in the payment form for the payment of contributions for injuries, you will have to use a different application format.